Office vacancy rates in central London are falling, pointing to a recovery in demand for workspace after the pandemic. But the rebound is uneven, with companies increasingly favouring newer, high-quality buildings while older offices struggle to attract tenants.

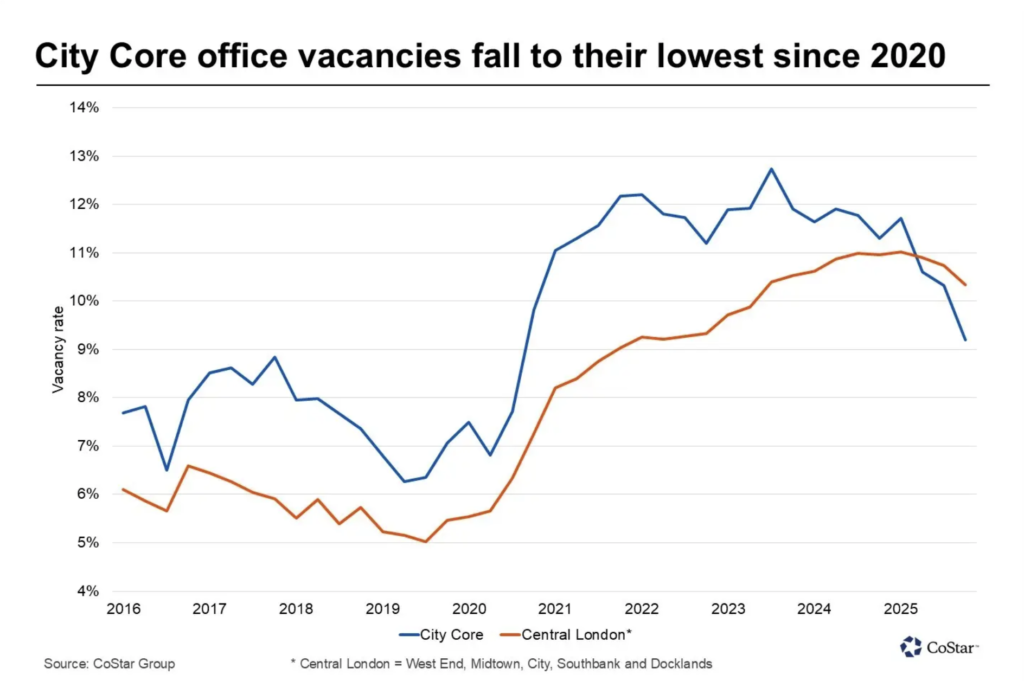

In the City, vacancy rates have dropped to around 9.2 per cent, a five-year low, according to CoStar data published on 26 February, as demand concentrates in prime locations and top-tier developments.

The trend highlights how vacancy rates have evolved in the City compared with the broader central London market, where availability remains higher in less central or less modern stock.

While vacancy rates are falling, the recovery is not uniform across the market.

“We’re seeing a real polarisation in the market between the best and the rest,” said Victoria Bajela, director of commercial research at Savills.

Since the pandemic, companies have reassessed what they want from office space. Hybrid working has reduced the need for sheer volume, but increased the importance of quality. Employers are focusing on spaces that can bring staff in rather than simply house them.

That shift has reinforced demand for central locations, where transport connectivity, amenities and proximity to clients remain key advantages. Areas such as the City core and the West End continue to attract occupiers looking to balance flexibility with presence.

Demand has been particularly strong in buildings that meet modern environmental standards and offer amenities such as collaborative workspaces, natural light and energy efficiency. Bajela said the vast majority of leasing activity is now concentrated in grade A space, with occupiers placing greater emphasis on sustainability, amenities and overall workplace experience.

Credit: @knightfrank on TikTok

The appeal of central locations is particularly evident in areas such as London Bridge, where connectivity via major rail and Underground links, alongside a growing mix of retail, dining and public space, has helped sustain demand. Developments in the area have increasingly been designed with mixed-use in mind, combining office, leisure and residential elements to create more dynamic commercial environments.

The question of what occupiers value most – location, quality or flexibility – remains central to how the market evolves. That combination is becoming a key differentiator in a more competitive leasing market. Locations that can offer both convenience and experience are proving more resilient, even as companies reduce their overall footprint.

At the other end of the market, demand has fallen sharply.

“There’s been a massive fall away in demand for secondary stock,” Bajela said, referring to older buildings that have not been recently refurbished.

These buildings, often characterised by lower energy efficiency ratings and fewer amenities, are increasingly being left behind. In some cases, they risk becoming what the industry calls “stranded assets”, particularly if they are in less central locations or lack the features now expected by tenants.

The challenge for landlords is not just finding tenants, but justifying the cost of upgrading older buildings to modern standards. Refurbishment can accrue significant costs, particularly to meet stricter environmental regulations and occupier expectations around sustainability.

What happens to those buildings depends largely on where they are and how viable they are to upgrade. In core locations, landlords are often investing heavily to refurbish or redevelop assets in order to meet demand. But in weaker areas, the options are less clear, with some buildings being repurposed, sold at a discount, or left vacant for extended periods.

Office-to-residential conversions are often cited as a potential solution, particularly given London’s housing shortage. But in practice, their role remains limited.

“It’s just not significant,” said Lucian Cook, head of residential research at Savills. He added conversions are unlikely to absorb a meaningful share of older office stock or materially increase housing supply.

That reflects both economic and structural barriers. Converting offices into housing can be complex and costly, particularly in buildings with large floor plates that do not easily lend themselves to residential layouts.

That view is echoed in the commercial market. Bajela said planning restrictions and structural constraints mean many office buildings, particularly in central London, are not suitable for residential use. Local authorities also tend to prioritise retaining commercial space in core business districts, limiting the scope for large-scale conversion.

Instead, much of the adjustment is happening within the office market itself, as landlords weigh refurbishment, repositioning or alternative commercial uses.

The shift is also changing how investors approach the market. Bajela said office ownership has become more capital intensive, with landlords needing to invest more heavily in upgrades to remain competitive.

“You have to invest in your asset,” she said, noting that expectations around quality and sustainability have risen sharply in recent years.

Those expectations are reshaping investment strategies, with capital increasingly flowing towards prime assets and away from secondary stock. For some investors, this divergence presents opportunity, particularly if older buildings can be acquired at a discount and successfully repositioned.

“We’re seeing continued demand for high-quality office space in central London, particularly in well-connected, amenity-rich locations,” said Hannah Smith, a PR manager at CBRE.

“Demand remains concentrated in best-in-class buildings, while older stock is taking longer to lease.”

Views on the future of office space remain mixed, with some firms continuing to prioritise flexibility and cost, even as demand for premium space strengthens. Hybrid working patterns are still evolving, and companies are continuing to adjust their real estate strategies accordingly.

But the direction of travel in central London appears increasingly clear. While vacancy rates are falling, the recovery in London’s office market is far from uniform.

Bajela said the shift towards higher-quality space is likely to persist, as offices evolve into places focused more on collaboration, experience and employee engagement.

“I don’t think the flight to quality is going to go away,” she said.

In that sense, the post-pandemic recovery is not simply about returning to previous levels of demand, but about a structural shift in what the office is for and which buildings are able to meet that need.