by Christopher McEvedy

https://drive.google.com/file/d/1WH0xUPIdz5LmytiGJy6osRQpklOsAy47/view?usp=share_link

The utility and wisdom of the EPL has been raised once more since the Israel-US war on Iran began, and the consequent rises in oil and gas prices.

The UK’s EPL was introduced by the Conservative government of Boris Johnson in 2022, in the wake of large energy company profits following Russia’s invasion of Ukraine, to respond to public concern by taxing excessive company profits, and also raise money to provide relief for consumers hit by cost-of-living increases, energy bills in particular.

The levy has been a source of controversy, with oil companies complaining about its prohibitive effect on investment, and even President Donald Trump weighing in at the most recent World Economic Forum meeting in an endeavour to castigate the trend of UK energy policy. On the other hand, a recent Climate Action Coalition and Clean Power Task Force report, citing YouGov polling data, shows that the thrust of the now Labour government’s energy transition and net zero policies retain a large degree of support among Labour, Lib Dem, and Green Party supporters.

What is the EPL?

The EPL is an additional tax imposed on energy company profits. Prior to its introduction, there was a 30% ring-fenced corporation tax, as well as a 10% supplementary charge. The first iteration of EPL added a further 25% in tax, which was increased to 35% in late 2022. This was increased again to 38% in 2023/24, and the headline marginal rate of tax in the EPL is therefore 78%.

Even without the EPL, development of hydrocarbon extraction from the North Sea faces significant hurdles. Labour has declared a ban on new licences. Zoe Avison, senior political advisor at the Climate Transformation voluntary sector organisation, Uplift points out that the controversial Rosebank field was licensed in 2001, but had no legitimate development consent, with the granted consent revoked in a judicial review decision in Scotland in January 2025. The process was deemed to have failed to include downstream emissions.

Imports account for 45% of UK energy needs, and within that oil and gas each account for 40 to 45%. Imported electricity (by interconnectors from various Northern European countries) accounts for the remaining 10 to 15%.

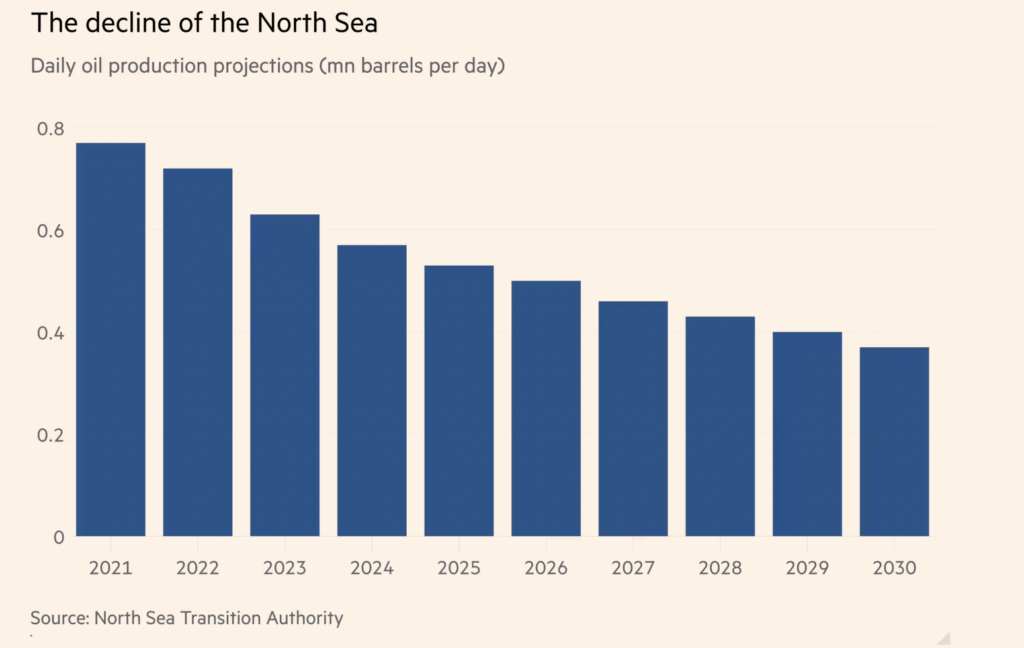

While the UK was an energy exporter from the early 1980s to the mid-2000s, as a result of the decline in North Sea production over time, alongside continuing high UK energy demand, it has been a net importer in the last 20 years.

Costs of UK energy imports, 2019 to 2025 in £ bn (ONS data)

| Year | Cost |

| 2019 | 60.2 |

| 2020 | 42.2 |

| 2021 | 73.7 |

| 2022 | 131.1 |

| 2023 | 100.0 |

| 2024 | 87.5 |

| 2025 | 78.2 |

Interestingly, costs of imported energy have remained significantly higher since 2022 than before.

Sanctioned tanker hit off Oman (screen grab from Reuters, 1.3.26)

A central question in the debate is whether hydrocarbons from the UK North Sea are any cheaper than those produced elsewhere. Both UK-produced and North Sea Norwegian pipeline gas are sold into the same wholesale market, NBP (National Balancing Point). They usually have a lower marginal cost than LNG imported from Qatar or the US, as well as continuous stable supply. However, the UK, like many European countries, has a pricing mechanism in which the most expensive energy source sets the price for the entire market – in this case including cheaper UK-produced or Norwegian-produced gas.

Those who argue that dropping the EPL would not impact gas prices in the short term are therefore correct.

The industry body, Offshore Energies UK (OEUK), argues that the EPL should be dropped this year, instead of in 2030 as is proposed. They point out that more than half of offshore energy companies have reduced headcount and many are considering leaving the North Sea altogether. They see EPL as a critical barrier to investment, and that profits have fallen to zero or even negative levels. They also put forward the view that the EPL risks energy security, as well as the argument that tax revenue would be higher with a reformed taxation regime, as well as bringing benefits to the wider economy, to jobs, and the supply chain.

Dr Mark Ireland, an expert in North Sea depletion, geology, and energy policy at Newcastle University, recognises that companies made huge profits after the Ukraine invasion, but says it is not really possible for them to exploit high prices: “They don’t really have much opportunity to be exploitative in that sense, because they sell it to someone at the price that’s determined by the contracts that they have in place.” Both Ireland and Zoe Avison agree that the Energy Price Guarantee introduced by Liz Truss’s government for consumers in late 2022, cost many times as much as any additional tax revenues generated by the EPL.

It is also accepted on all sides that since the EPL was introduced in 2022, profits of companies operating in the North Sea have decreased. Although Shell and BP are both multinationals, the profits of these two largest UK-based oil and gas majors show considerable variation over time:

Net profits for Shell and BP, 2019 to 2025 in USD bn

| Year | Shell | BP |

| 2019 | 15.8 | 4.0 |

| 2020 | -21.7 | -20.3 |

| 2021 | 20.1 | 7.6 |

| 2022 | 42.3 | -2.5 |

| 2023 | 19.4 | 15.2 |

| 2024 | 16.1 | 0.4 |

| 2025 | 17.8 | 0.05 |

Ireland points out “quite a significant change in the landscape of the companies that operate in the North Sea. Some people would say that’s due to the tax not being favourable, but actually even before things like the EPL, we were already seeing oil and gas majors reduce their footprint, which is a pretty normal thing to happen.” Professor Michael Tamvakis, City University, agrees that largely only smaller upstream companies, those without refining or distribution activity, remain in the North Sea.

Dr Ireland, Professor Tamvakis, and Zoe Avison all recognise that the North Sea is a declining basin, and Professor Tamvakis suggests it has perhaps another 10 years of extraction potential.

The comparison with Norway in terms of exploration is interesting.

Exploratory (‘wildcat) wells drilled

| Year | UK | Norway |

| 2021 | 5 | 27 |

| 2022 | 8 | 31-35 |

| 2023 | 12 | 34 |

| 2024 | ? 0 | 42 |

| 2025 | 0 | 45 |

| 2026 (projected) | 0 | c. 37 |

Sources: Financial Times, Westwood Energy, Offshore Energies UK

Ireland says that, “As a geologist, the first thing I would point to is that we might share the same body of water, the North Sea, but the geology is not identical,” particularly further north off the coast of Norway. But he and Professor Tamvakis point to the fact that the Norwegian state has majority ownership of the principal company operating in the Norwegian North Sea, Equinor (formerly Statoil). Ireland points out: “That does seem quite important in the kind of mood music, if you like.”

Professor Tamvakis observes that the UK has historically assumed plentiful gas supplies, relies on gas more than many European countries, and yet has almost no storage capacity: “We don’t have a very large storage capacity, a few days basically.” He compares this to the situation in Germany, which also uses a lot of gas, but has “hundreds and hundreds” of storage facilities. Mark Ireland points out that the main storage facility, responsible for 70% of UK capacity and run by Centrica, has been “managed fairly appallingly”. In fact, it has been closed because of safety concerns and high maintenance costs for five of the last nine years, and now operates at reduced capacity.

There is a plan to replace the EPL with an Oil and Gas Price Mechanism (OGPM) in 2030, which will be threshold-based rather than a blanket tax on company profits. Interestingly, and although they may differ as to the thresholds in the OPGM, all sides including the producers’ body and the environmental organisation – agree this is the way forward, even if they disagree about whether the country should wait another four years for this change.

Sources

Dr Mark Ireland, an expert in North Sea depletion, geology, and energy policy at Newcastle University

Email: Mark.Ireland@newcastle.ac.uk

Interview: 26.3.26

Professor Michael Tamvakis, Professor of Commodity Economics and Finance at the Bayes Business School City St George’s University of London

Email: M.Tamvakis@citystgeorges.ac.uk

Interview: 25.3.26

Zoe Avison, Senior Political Advisor at the climate transformation voluntary sector organisation, Uplift

Email: zoe@upliftuk.org

Interview: 27.3.26

You don’t necessarily have to publish it just yet go back so if you want to keep working on it later on you would go back and just hit test again, and then when you’re ready to just publish it,